Accepted Contracts Up 86% in 5 Weeks

The Phoenix housing market update for February 2023 below has been provided by The Cromford® Report. It features the stats you need to know and explains what they mean if you’re thinking about buying or selling a home right now.

If you would like similar information about the real estate market in a specific city or zip code within Greater Phoenix, let us know! We’d be happy to send it to you.

What does this mean for Greater Phoenix home buyers?

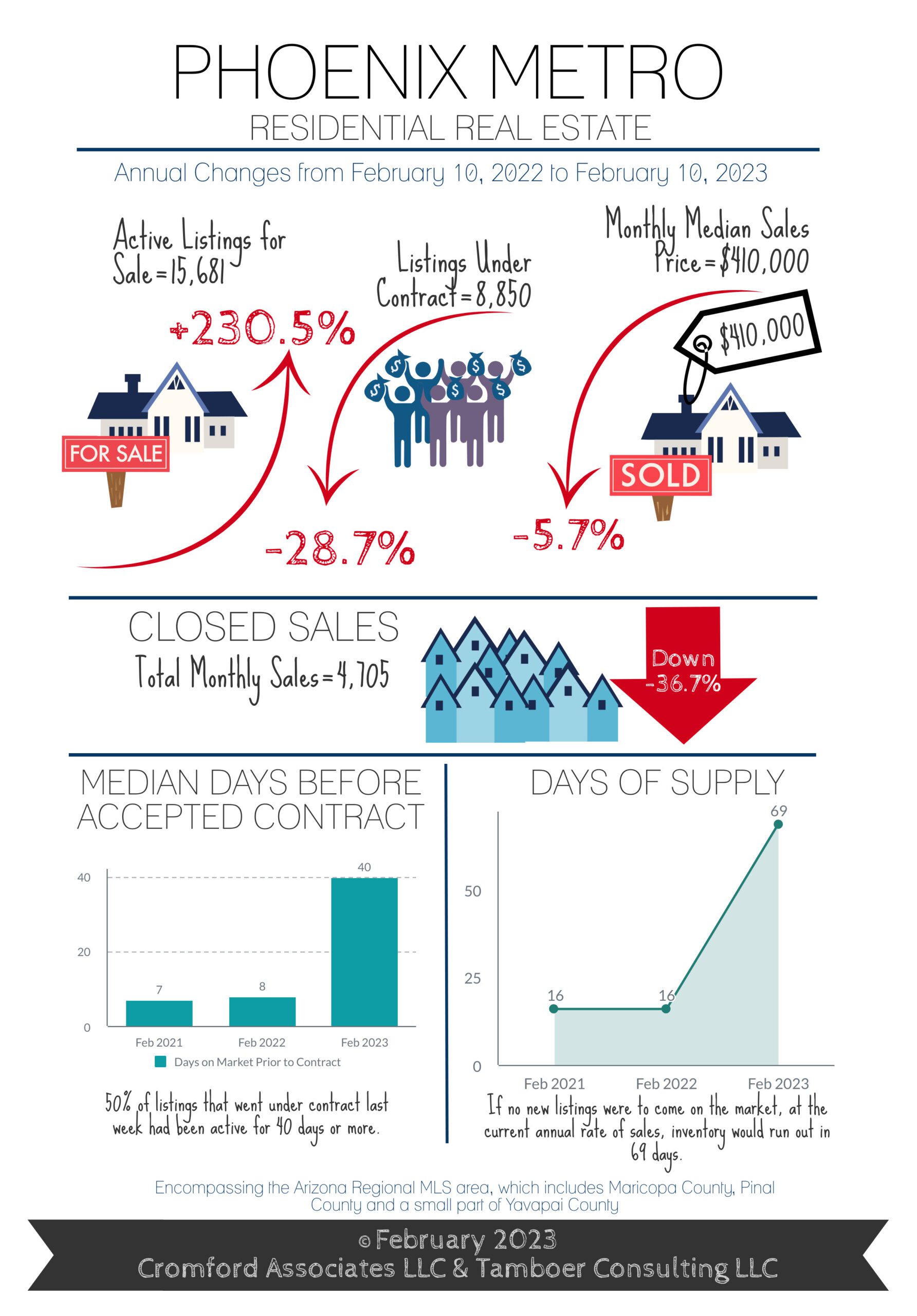

The spring season is upon Greater Phoenix. February hosts the Waste Management Open and Super Bowl LVII this year, putting the metro area in the national spotlight more than usual during our peak season for weather, tourism, and buyer activity. This, combined with mortgage rates briefly stabilizing between 6.0-6.2% in January, contributed to an 86% increase in accepted contracts since the beginning of the year. Six major cities moved out of balanced markets into seller’s markets over the last 4 weeks: Phoenix, Avondale, Glendale, Tempe, Mesa, and Gilbert. Two cities came out of buyer’s markets into balance: Peoria and Surprise. Only Goodyear, Queen Creek, Maricopa, and Buckeye remain in buyer’s markets at this stage. Now 11 out of the 17 major cities are in seller’s markets, but much weaker ones compared to the last 2.5 years.

The shift is in its early stage and fragile, however, and could fall back to balance if mortgage rates become too volatile. Rates remain unpredictable, but that doesn’t stop the industry from trying to predict them.

Multiple outlets, such as the National Association of Realtors, Mortgage Bankers Association, Freddie Mac, Fannie Mae, and CoreLogic, released expectations in January that mortgage rates will either stabilize or trend down in the first quarter of 2023. Very few are predicting rates to increase this year overall, but we may see them bounce around as the bond market flinches with every report on inflation and employment. This may cause buyer demand to ebb and flow over the next few months, too. Speaking of employment, the latest report for Arizona showed an increase of 93,700 jobs for the state over the course of 2022. In Maricopa County, the unemployment rate dropped from 3.1% in January to 2.7% by the end of December, continuing to outperform national measures. Even as the labor force grew by nearly 58,000 people, even as layoffs swept the real estate and tech industries, people claiming unemployment declined by 9,500 over the course of 2022. Private sector earnings also grew by 4.1% year-over-year, a positive indicator for housing affordability to improve in Greater Phoenix.

What does this mean for Greater Phoenix home sellers?

Don’t be fooled by this seller’s market, it is nothing like the seller’s market of early 2022. Sellers may notice there is less pressure for a price reduction as there are few new listings entering the market. There were only 9,664 new listings added to the Arizona Regional MLS since the beginning of 2023, the lowest number of new listings measured in at least 23 years. The median is 14,000 listings, and the highest measured was over 21,000 in 2006 over the same 5-week time frame. Less competition is good for price stability. Sellers may notice fewer days on market prior to contract. Half of owners who accepted contracts last week were on the market for 40 days or less (listed after January 4th) compared to the peak of 56 days in December.

In a weak seller’s market like this, as we shift into the Spring season, days on market prior to contract may settle in at 25-30 days; a far cry from the 5-7 days in early 2022. Sellers will notice little change in negotiations or concessions at this stage.

Last month, 51% of sales involved seller concessions to the buyer with a median cost of $9,700. So far in February, 47% have involved concessions at a cost of $9,800. The average negotiation is 2.8% below the last list price, down from 3.5% last month. Sales measures rolling in now are reflecting contracts written in late December and early January, which was a mixed bag of cities in balance and cities in buyer’s markets at the time. The effects of the current seller’s market will not be seen in sales price measures until March, at which point we expect to see the rate of decline in sales price measures either slow down or stabilize. Mortgage rates could change the game quickly, however. It’s not a time for buyers or sellers to take market conditions for granted.

Conclusion

Whether you’re a buyer, seller, or investor, The Hill Group has the experience and strategies to help you reach your real estate goals this year. Let us know how we can help! If you’d like to receive these monthly market updates as soon as they are posted, subscribe to our email newsletter. For a free home value estimate prepared by our team, simply type in your address here.

Commentary written by Tina Tamboer, Senior Housing Analyst with The Cromford Report

©2023 Cromford Associates LLC and Tamboer Consulting LLC