Buyers Have Been More Reactive to Mortgage Rates Than Normal

The Phoenix housing market update for December 2022 below has been provided by The Cromford® Report. It features the stats you need to know and explains what they mean if you’re thinking about buying or selling a home right now.

If you would like similar information about the real estate market in a specific city or zip code within Greater Phoenix, let us know! We’d be happy to send it to you.

What does this mean for Greater Phoenix home buyers?

Buyer demand has been more reactive to mortgage rates than normal, but that’s to be expected at the rate of increase we’ve seen this year. In terms of affordability in Greater Phoenix, a household making the median family income should normally be able to afford 60-75% of what’s sold. That measure for the 2nd and 3rd quarters of 2022 was only 22%. Some believe it would take years for affordability to return to a normal range unless sales prices drop dramatically, but that’s not necessarily true. As rising mortgage rates have quickly pushed affordability down, declining mortgage rates can quickly push it back up.

Affordability is determined by 3 things: family income, 30-yr mortgage rates, and sales price.

Price is not the only factor that needs to change in order to push affordability back to a normal state. For example, in order for the current median sales price of $418,000 to be considered affordable to a family making the median income of $88,800 in 2021, mortgage rates would have to drop to 3.35%. Or, the median income would have to increase to $119,000 per year. Both of those scenarios are too extreme to expect in a short amount of time. However, it’s reasonable to believe they will meet somewhere in the middle in 2023.

HUD will not release updated income measures for 2022 until May 2023. However, according to the AZ Department of Economic Opportunity, year-over-year wage income has shown a 5-8% increase each month through October. If we estimate a total 7% increase in median family income, that results in a median of $95,000 per year. With 10% down, that puts a family’s budgeted purchase price of a home around: $335,000 at a 6.3% rate, $368,000 at 5.3%, and $406,000 at 4.3%.

From this example, we can see that mortgage rates have a stronger chance of reversing affordability issues faster than any other factor and can mean the difference between a 20% drop in prices and a mere 3% drop. The only experts who can accurately predict the direction of sales prices are those who can accurately predict mortgage rates. However, at this stage, mortgage rates are still volatile and most predictions have been flat-out wrong.

If rates rise, prices will have to drop more to reach optimum affordability. If they drop, prices will not have to drop nearly as much. The best advice for buyers is to stay engaged with where rates are on a daily basis and be fully educated on lender programs and seller incentives available so that they can be the first to act when the property and the payment are right for them.

What does this mean for Greater Phoenix home sellers?

Welcome to an official Buyer Market in Greater Phoenix, albeit a weak one, for the first time since 2010. As expected, the city of Phoenix finally succumbed to a Buyer Market in mid-November, thus classifying the entire market as such. (The northeast cities of Paradise Valley, Scottsdale, Fountain Hills, and Cave Creek are all still either Balanced Markets or mild Seller Markets.) While market indicators were plummeting from an extreme Seller Market to Balanced between March and June, the trip from Balanced to a Buyer Market from July to December has been more like a gentle glide.

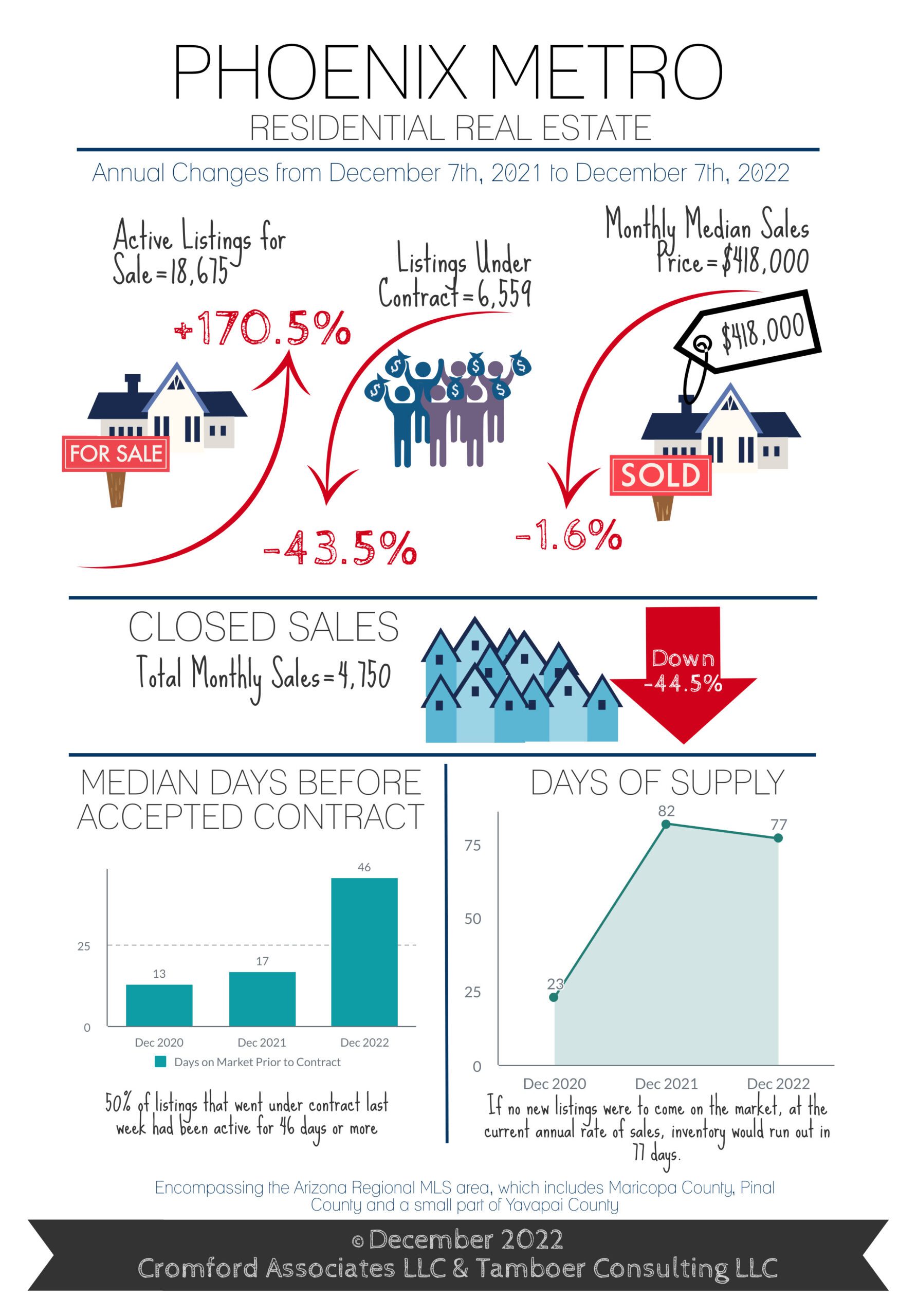

Price responses didn’t wait for the official calling; median sale prices began showing a decline after May and as of this date are down 12%, essentially erasing appreciation gained since November 2021 and resulting in a 1.6% negative year-over-year median change. From here on out, expect reports of negative annual appreciation rates every month as each measure will now be compared to the first half of 2022 price measures.

Moving into 2023, even if mortgage rates stay the same, it is expected that contract activity will increase seasonally as it does every year.

Rate buy-downs will remain a key factor in buyer incentives unless rates decline. However, after a long 4th quarter sellers should be able to enjoy more traffic, fewer days on market, and serious buyers in the first half of 2023.

Conclusion

Whether you’re a buyer, seller, or investor, The Hill Group has the experience and strategies to help you reach your real estate goals this year. Let us know how we can help! If you’d like to receive these monthly market updates as soon as they are posted, subscribe to our email newsletter. For a free home value estimate prepared by our team, simply type in your address here.

Commentary written by Tina Tamboer, Senior Housing Analyst with The Cromford Report

©2022 Cromford Associates LLC and Tamboer Consulting LLC